The future is often not as we think

What if the entire automotive eco-system changed in a matter of a few years? It’s time to explore the unthinkable. There is a confluence of powerful forces right now, and it’s happened faster than many in Europe or the UK thought possible.

Great ideas do not last forever

The entire business including collision repair revolves around vehicles – who’s making the best, the most popular, the most fashionable. Each company goes through a series of growth spurts as a new idea, a new angle or new product gives it an advantage over the competition. What happens when those growth spurts become very small?

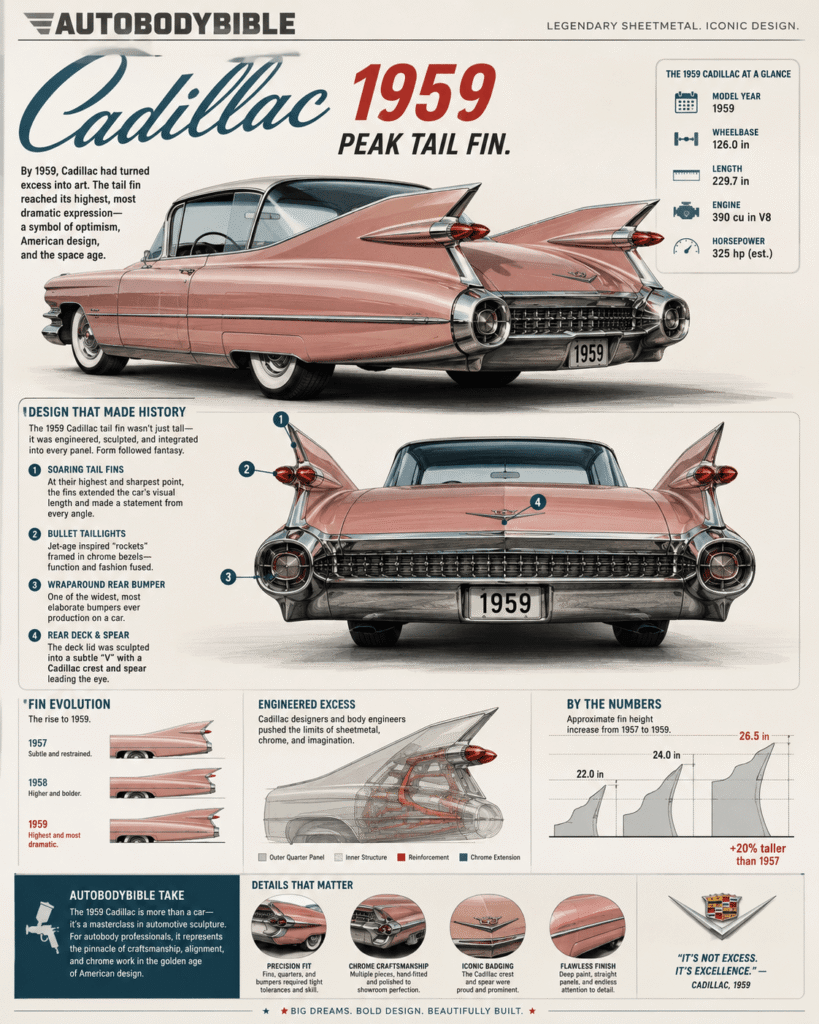

Consider Cadillac in 1959 – peak tail fin.

The formula was a very large, high torque, low speed engine on a chassis, driving the rear wheels with a body that changed at least twice a year. Underneath the running gear frequently featured cross-ply tyres and drum brakes even though by the 1970s better technologies were available. These were relaxing mobile living rooms designed to travel for 10 or more hours at a time with inexpensive gasoline.

However, for those who cared to see, the storm clouds were gathering. In Japan, they had been assisted by many USA companies to re-start their manufacturing sector, and so understood the key advantage of thinking bigger. This was combined with vehicles which were inherently smaller, and so able to access many, many more global markets.

Most countries outside of the USA developed inherently more efficient powertrains, so although the 1973 oil crisis – the birth of OPEC – hit the global economy hard, it hit the USA hardest. The ‘big three’ – GM, Ford and Chrysler – continued with the highly profitable vehicle formula, even though it restricted the markets that could take their products in volume.

Each of the companies tried to correct this – GM with the X-body platform in 1979 and the Saturn division in 1991, for example – with limited success. Re-directing a very large company takes a lot of money and a long, long time.

The entire European automotive business is in that same rut now. For many reasons the highly profitable exports to China have either stopped or ben dramatically reduced, and not replaced with significant demand from other parts of the world. Each manufacturer works incredibly hard to make competitive products, but if one can only see a short distance, the overall view maybe limited.

In short, it is complacent.

Reasons to be happy…

The European vehicle manufacturers famously had enough spare factory space to make more than a million vehicles back in the 1990s, and even more by the early 2010s. By then the economic reality of the great financial crisis had already pushed companies to do the unthinkable – selling their trade mark and selling historically significant sites. By 2024, the sector had matched capacity to demand with an average plant capacity utilisation of around 80 per cent (lowest was 67 per cent, highest was 95 percent utilisation).

From 2024 to 2026 the plant capacity gap re-opened. Stellantis in Europe have at least 4 plants which need to close or be sold off, with a further plant dedicated to the circular economy. Ford have already closed key European plants and now consider giving their best assembly line of 3 in Valancia to the highest bidder, along with talk of closing Cologne. All three German headquartered groups are also considering plant closure or sales.

This is the effect…. not by 2035, not by 2030, but 2026…

Key actors included:

- Massive write-downs for electrification

- Stalled battery manufacture in the EU27 and UK

- A political drive to Net Zero at odds with the rate of market acceptance

China – massive manufacturing capability

The development of a 27 million a year manufacturing operation with rolling 5-year national development plans a total of 40 years to deliver, is a qualified success. The internal market is locked into its fourth year of a ruinous internal price war, which means the profit per car is tiny. The only way to make a decent profit is to export in volume – each vehicle sold in Europe represents the profit of many of the identical vehicles sold in China.

Export is a priority: 11 per cent of EU27 plus UK market share in less than 2 years…..

Factory space, including existing production capacity is around 50 million vehicles per year (half the global output of new vehicles) which was funded by provincial and central government along with state backed banks.

Guess who is being offered entire European factories?

Yet, why would China need European factories when it already has factories and as the biggest ship builder in the world, it has a growing fleet of car transporter ships?

Consequences

If the China manufacturers achieve 30 or 40 per cent EU27 plus UK market share (domination), what could happen? The transporters arrive full of new cars, and might leave empty. Or full of vehicles to be repaired / recycled. By the way, some of the biggest container shipping lines in the world are based in China. In addition, China labour costs are still lower than EU27 or UK

Will damaged vehicles stay in the UK? Why process high-demand rare metals away from China, the biggest Li-Ion manufacturer in the world?

The key question: How should we respond?

{kind=link}