The politics rolls on, and collision repairers get more exposed to risk

Bodyshop News Australia published a status about the European automotive business and the effect of massive exports from China last month. Australia, much like Europe, has relatively static car sales levels – it’s not going to be a 5 million car a year market anytime soon. So, as the China based OEMs sell multiple variations of SUV with multiple brand labels, they join a market which has been selling smaller number of more models each year.

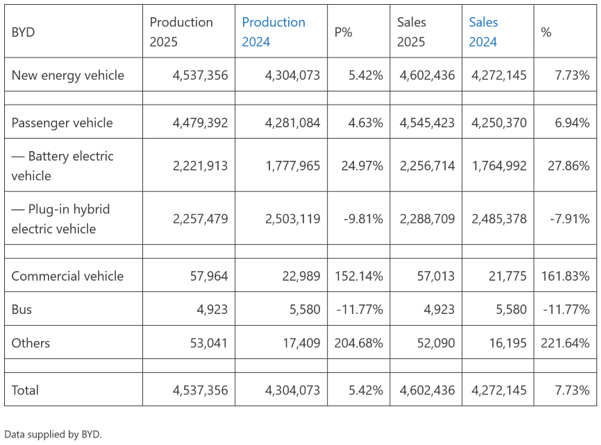

Consider the numbers from BYD:

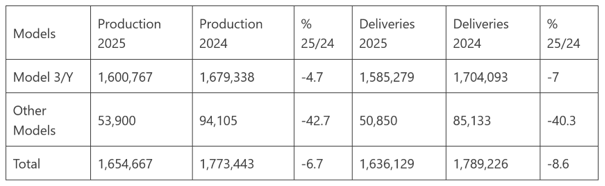

Tesla sales for 2025:

Tesla production for 2025:

Remember this:

- BYD expended it’s overall production by roughly 1 million units per year for three consecutive years… until 2025.

- The vast majority of BYD vehicle output is cars.

- Of those, PHEV accounted for roughly half the car sales, although the up-coming economic belt-tightening in China should reverse this slight dip in growth.

- Tesla’s biggest single factory is in Shanghai, where it uses unique ADAS systems for domestic sales compared to USA based technology for rest of world exports. Further, every single dollar earned by exports from the Shanghai factory remains in China, by contractual obligation.

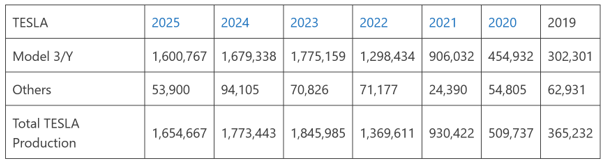

It shows what we’d thought of as a ‘start up’ – Tesla – compared to an even more extensively funded version, BYD.

Is China a power house – or just trying to make a living?

In a huge and growing market like China, or the long-promised ever imminent car ownership growth in India, there is good reason to buy a complete vehicle, white label, and place it in those markets. The risk is low and the profit should be good.

China has long standing problems of private investment property market ‘slight falling over’ which is directly linked to vast over capacity in the domestic automotive manufacturing sector, happening as the automotive market enters its fourth consecutive year of vicious new vehicle sales competition combined with removal of subsidies for some powertrain types. The upswing to buy China vehicles because the apparent quality, apparent reliability and very competitive pricing eclipses any vehicle imported or built in China by a foreign company – has just run out of steam.

Hence the rush to keep production rolling, keep the endless flow of identikit SUV ‘new’ models, just to keep paying for loans on excess manufacturing capacity. Even with severe disruption in the Middle East during 2026 means a ship load of vehicles landed in Australia are demonstrably more profitable than if sold in the China domestic market.

So, what are the problems?

- More models and with even more variations chasing fewer sales per model, per year compared to the ones they replace.

- Over reliance on home-grown software, non-standardised major components and manufacturers specific structured repair information – it was always so, but the number of models makes this situation worse than ever before.

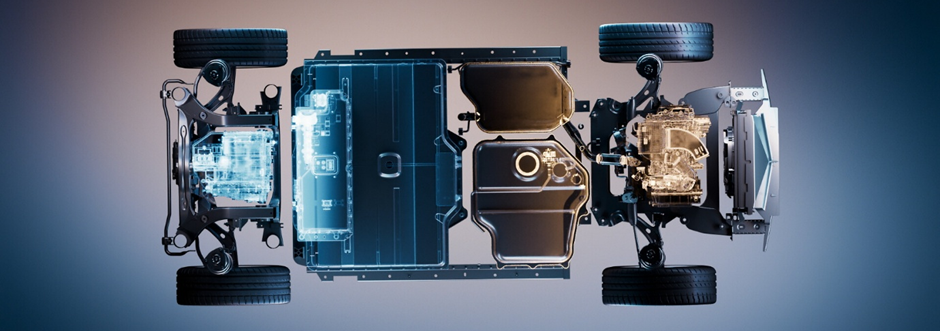

What are the most valuable bits of electrified powertrain?

We are learning that with human drivers and mixed traffic conditions, use as well as frequency / type of charging affect the loss of energy storage capacity. Whereas an internal combustion engine health can be determined by use of a few parameters due to the century of knowledge each parameter represents, some of which read across to electric powertrains (lubricant technology for example) the number of unknowns, the lack of data, is more marked with electrified powertrains, but not for much longer as more vehicles generate more information.

The highest value parts, the easiest to assess in terms of remaining service life are the power control electronics, the traction motor and driveline.

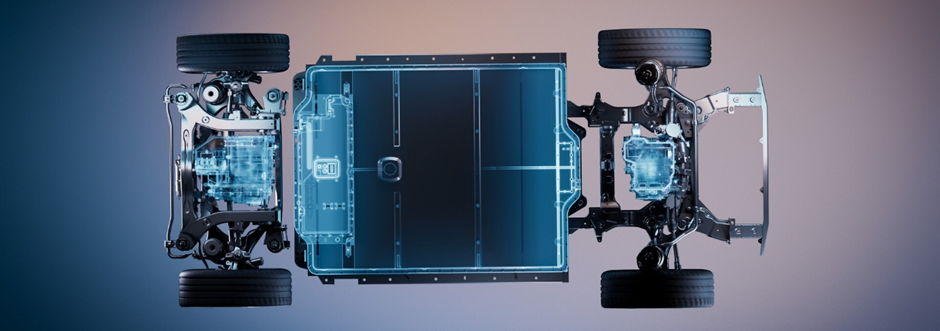

Traction batteries

In the near term these remain the biggest risk for repairers and insurers. The riddle is:

‘What’s worth nothing – or even costs – after impact, but costs almost all of the residual value to replace? A traction battery’.

Vehicles with large traction batteries seem to be hammered – I think falsely – in terms of residual value. As discussed previously quantifying how much life is left in a used battery pack is a challenge given it is difficult to manage each cell thermally. Hence the HV traction battery is built with cells with as close to identical performance as possible, so the degradation is uniform and the risks of overloading any single cell are minimised.

Things are moving quickly to ensure a damaged or defective HV traction battery, which could be supplied new for upwards of four times the manufactured cost of US$ 72 per kWh, could be refurbished. This leads directly to more precise recycling of the defective components, and prevention of the cell level imbalance that might initiate thermal runway.

- The cost of a 100 kWh battery should be circa US$ 7200 for the most common Li-Ion electrolyte, anode and cathode cell combinations, which can retail for anything upwards of US$ 28800. Newer and better battery technologies cost much more until production volumes increase.

- Insurers know there isn’t a lot of quality information to use if the pack should be replaced or repaired, and also know HV traction battery repairers are not yet common either.

- Insurers also know the HV traction battery will survive the impact (front, side or rear) but could get hit from the underside in subsequent collisions after the initial impact.

The packaging of the HV traction battery, especially on a battery electric vehicle (BEV) or a range-extender electric vehicle (REEV), is super critical in terms of;

- height, since the sides are defined by the engineered allowable intrusion for the ANCAP side impact tests,

- the front is defined by the engineered impact load transfer for the ANCAP front impact tests,

- the cabin height is defined by the 95-percentile size of the target market,

- the underside is defined by the ground clearance line.

- the rear is defined by engineered load transfer from type approval and internal manufacturer impact test standards.

The HV traction battery is literally boxed in. Addition of full-length skid plates is possible if there is some latitude on the ground clearance line, but really needs gapping from the lowest face of the HV traction battery so as the skid plate contacts and bends, it does not press into the battery it’s trying to protect. If the latitude is not there, the HV traction battery internals need to be made smaller.

Renault vision of the future: Top, the frame, which can be altered for length and width. Middle: REEV, with internal combustion engine for the front drive and traction battery / rear electric motor to provide 4-wheel drive. Bottom: A larger traction battery with either a rear drive motor or two drive motors. This jumps back to the days of perimeter frames, by linking both subframes to the central carrier.

What’s next for traction batteries?

Much like fusion technology, solid state and / or solid electrolyte batteries are full of promise in terms of energy density and resistance to internal shorting, but the technology has been ‘just around the corner’ for at least a decade. When it does finally appear, it is likely to be not inexpensive, nor significantly safer than a well built and well operated conventional Lithium-Ion cell pack.

There are interesting questions about how charging systems could be much, much common and much, much easier to use. This could lead to the reduction of the 100 kWh giant packs down towards 60 kWh, which makes the whole packaging issue far more straight-forward. Similarly, for vehicles with a range of circa 200km, a battery pack offering 30 kWh of energy storage would be less expensive, easy to package and inherently lower risk in the event of catastrophic impact damage due to the lower levels of stored energy.

What is the European Commission doing about this?

The EU27 Commission creates the law approved by member states which becomes part of the new vehicle type approval process, without which no new vehicle can sold. The UK and other counties outside the EU27 adopt these laws, or mix them with similar law from the USA, South Korea or Japan as well as creating their own standards.

The EU27 Commission became aware the tail pipe emissions law, the incentives for battery electric vehicles along with the internal market for ‘carbon credits’ had left the vehicle manufacturers in member states weighed down with extra direct costs. Further, imports from China took advantage of the consumer incentives but side stepped the extra direct costs.

The EU27 Commission were really rattled by Dacia Spring, which was originally engineered in India with a core of Renault and Nissan engineers to become Kwid. The project was then turned into a BEV by a Renault Nissan team in China, and then exported the cars from there back to Europe. This was the cheapest BEV on the market, with BEV centric mandates set by the EU27 Commission.

The conundrum. How to keep trade, prevent import of complete vehicles but not upset China.

The EU27 Commission went on tour starting at the end of 2024, and gathered lots of ideas from all over. The result was to be published in December, January, February and then it did finally appear as a definite maybe to start discussions in March 2026. Once again, the dreaded EU27 ‘carbon’ credit trading scheme features, leading to all sorts of tiered effects and taxes.

In effect, nothing has been done, and the wave of product coming in from China gets bigger every single day. The manufacturers in the EU27 and UK do not agree with what should be done, but all are aware right now the main source of all the parts and materials required to make electrified powertrains come from China.

There is so much pressure to move supply of processed raw materials and finished products from China, but time is against the rest of world, given China has a massive, massive manufacturing capability right now.

For collision repairers

The effect of all of the above will be:

- New skills to not only assess HV traction battery condition, but where possible the ability to strip, replace certain components, rebuild and verify the repair.

- Realisation that even if a platform is used by many different models, the number of a certain make / model / body shape will decrease, and the collision repair parts will not be supported for as long after production stops. That drives news skills to source parts, get parts made and even do some of that within the business.

- New skills to support ever evolving software, and to support vehicles left behind as their software becomes unsupported. After all, a vehicle is rather bigger and more complex than a phone, so it’s not going to get thrown away so easily (I’m looking at Apple…..).

Regularising automotive engineering is not going to happen very much even withing a single vehicle manufacturer. While we get some wins via platform use across different brands, in the main the day job in collision repair is going to present a significantly increased variety of models with in effect shorter life cycles…. unless we can prevent that.

Isn’t that a better ecology solution to just throwing whole vehicles away?

Source of sales numbers: Tesla, BYD and www.best-selling-cars.com

{kind=link}