We’re going to look into how events are shaping the automotive business. Let’s consider the chaos in Europe caused in no small part by mandated battery electric vehicles (‘BEV’) along with the politically driven agenda to purge the internal combustion engine…. at the very same time the ‘overnight success’ of China which has taken 40 years, finally arrived in Europe.

Firstly China

For many years China set the objective of building a domestic automotive sector capable of not only serving the domestic market but also for export. All sorts of routes were tried, leading to many mistakes along the way. Incentives were offered by provinces and domestic banks to ‘invest’ in the automotive sector. The result was extensive factory buildings operating far below capacity with products that were until around 2010 not quite world class.

One part of the plan that did work was to partner with non-China manufacturers, allowing up to date models to be built for China and to be exported too. Famous ‘foreign’ manufacturing partnerships included GM, Ford, Mazda, Honda, Toyota, Mercedes-Benz, Volkswagen Group and BMW.

Since that time the wider China economy has been transformed with significant increase of wealth for many. For the automotive sector this meant domestic demand increased significantly, along with integration of domestically designed / developed electronic systems into vehicles. This enabled fresh models with world class build quality.

Bigger is better

In 2024 the China automotive sector had:

- Production: 26.76 million cars, 3.1 million LCVs and 0.99 million HGVs per year.

- Factory space / capacity close to 55 million units per year.

These numbers seem not to include e-scooters.

China has few significant manufacturing facilities outside the country – so out of 75.5 million units built globally in 2024, around one third came from China. Will 55 million vehicles come from China eventually? No. Long ago most manufacturers understood it was way more cost effective to ship high value parts around the world rather than complete vehicles which contain a significant volume of air.

Investment in new products took off from around 2010, feeding an ever-expanding market. The point where domestic brands were no longer seen as a low-cost alternative to imports or foreign company joint ventures built in China occurred around 2018.

China market peak profitability arrived around 2023, but there has been a massive internal market price war since then which has affected domestic, joint venture as well as foreign imported vehicles, with some international players such as Jeep electing to leave the market altogether.

With diminishing profitability in the domestic market, China automotive manufacturers have pushed for exports for to key markets in the EU27 and UK, expanding on conquests in the Norway (128,000 cars in 2024) and select African / Middle East markets. Why is export so important? Foreign exchange. Each vehicle sale realises a higher price than the present domestic market, and provides vital alternative currencies.

The warnings

The China national government has issued many rolling 5-year strategic plans, expressing frustration with the modest returns for 40 plus years of support. Vehicles being built for export with almost no idea of how they would be sold. No brand. Just product.

The rebuke was to not to just fill up ships with vehicles but to start thinking about why conquest markets should buy those vehicles.

Early in discussions about EU27 tariffs for China built battery electric vehicles, BYD stated that even a 10 per cent import duty in addition to existing taxation could be taken without raising retail process and still turn a profit. The EU27 manufacturers knew full well that their margins are closer to 5 per cent, and so could not consider taking such a tariff without price increases for the consumer – a sobering moment.

EU27 Commission and law

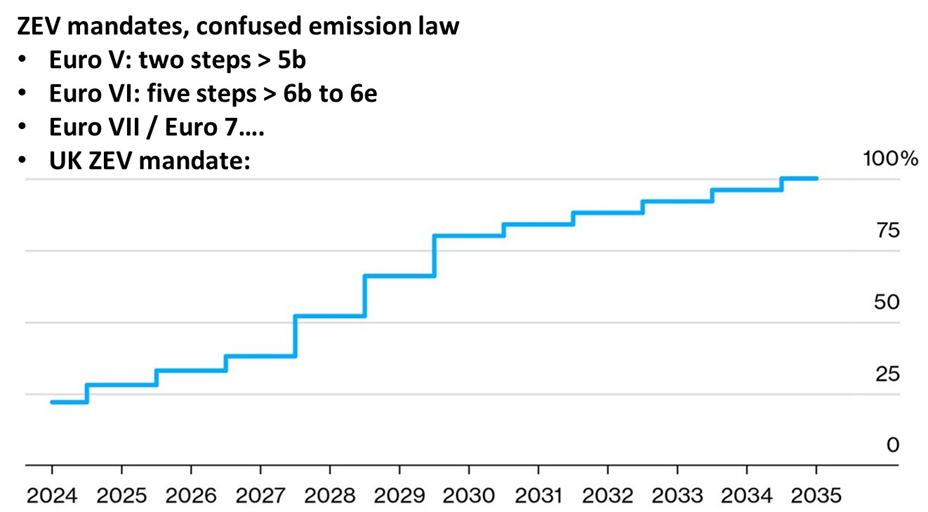

As China found its feet, so the European tail pipe emission laws stumbled through – too late, too costly, too complex. Yet, at the same time, the very same people making laws are trying to ban some types pure internal combustion engine powertrains and promote BEVs without anywhere near enough infrastructure.

New model programmes were doubled or even trebled to address all the electrified and pure electric powertrain options. For EU27 manufacturers the burden of this activity against an ever-tightening time scale before taxation for producing the ‘wrong type’ of vehicle caused lasting damage. The manufacturers had enough – Euro 7 was publicly declined. The legislation was once again late, once again confused and now had a 3 year-ish life span before internal combustion engine phase out started in 2030.

The EU27 commission were not amused, but sat up when Germany, France and Italy pointed out the rejection was valid.

The confluence and some danger

On the one hand China has control of mining, processing and supply of key materials required for any sort of electrified powertrain, along with one of the largest domestic markets in the world. Yet, apart from SAIC via MG Motor and Maxus, for many years most of the China automotive sector was unknown to most of Europe.

The impact of purging the internal combustion engine powertrains, the incomplete infrastructure roll-out to support battery electric powertrains, the tripling of each new model introduction all served to slow down the European automotive sector, and helped China prepare to take market share by storm.

There is a large demand in China for basic transportation – vehicles that are seemingly well equipped with airbags but are closer to a quadracycle than a car. These products are already made in large volume, are very useful for running around, and could be sold at a profit with all duties paid for less than £10000. A lot less.

China is testing EU27 law for ultra-light vehicles – and if successful, will send many, many vehicles to Europe. The EU27 commission have known about the quadracycle problem for years, and some of the European built vehicles do not have front or rear end crush structures let alone airbags. If such inexpensive vehicles are released on the open market the result in congested towns and cities will make some sense – but no sense at all for use on higher speed routes.

Regardless of vehicle size, price cutting will bring the economic write-off point much closer to the first registration, possibly just a couple of years. Without radical engineering to make repairability inherently cheaper – something all manufacturers should consider – there is a risk more vehicles than ever before will be recycled not too long after they were first sold.

The first major casualty will be the franchised dealer. Already the main profit comes from used vehicle sales and servicing, and these activities do not need expensive brand themed buildings. The opportunity for collision repairers? To host vehicle sales direct to consumers, to repair vehicles – to take some ‘land grab’.

Conclusion

On top of everything else, assessors will have to contend with new brands with a gaggle of models which have already been on sale for few years in China and supporting documentation which getting better with each new release. The vehicles are no less complex in any way than existing European products. The difficulty will be the effect on residuals which may accelerate the number of write-offs.

As never before, adherence to the law and application of knowledge by IAEA members will be very important not only for the damage assessment but the overall repair process.

Renault Twingo E-Tech revealed in production form on 6th November 2025: Based on the R4 and R5 BEV platform, with reduced parts count and a circa €20000 retail price. Will this be enough to answer the China challenge?

{kind=link}