International tariff wars – what could be the outcome?

The UK just about five decades agon was the biggest producer of buses in the world, and among the biggest heavy truck manufacturer in the world too. The UK car industry was awash with models. Of course, this disappeared through lack of investment and huge, huge errors. It was painful.

For the EU27 and UK we now face the consequences of actions planned more than 17 years ago, as fresh internal combustion Euro 6e regulations– in three stages – and proposed internal combustion engine bans bit deep at the very same time BEV sales mandates bite. The ‘house’ is fully ablaze on the roof.

With the trade war between China and the USA in full play, EU27 plus UK is seen as a mere cash cow and collateral damage at the very same time. In effect, the house has a fire underneath it now, as the USA and China compete to undercut the regional vehicle manufacturers.

Excess manufacturing capacity, high-cost staff

The EU27 has struggled with excess manufacturing capacity for many decades, never quite getting around to trim back plants. The UK went through the brutal process back in the era of Mrs Thatcher with mass bankruptcies, but the EU27 and Germany in particular were spared this. The UK like Australia knows full well that the loss of manufacturing weakens the representation, and even the importance of the market.

Mazda, for instance, will sell the Mazda6e by the middle of 2025 in Europe, even though it’s been on sale in China since the end of 2024 and as a Changan Auto model since 2022. It’s all part of the adjustment as Europe seems to lose influence – ‘here’s something we made earlier’.

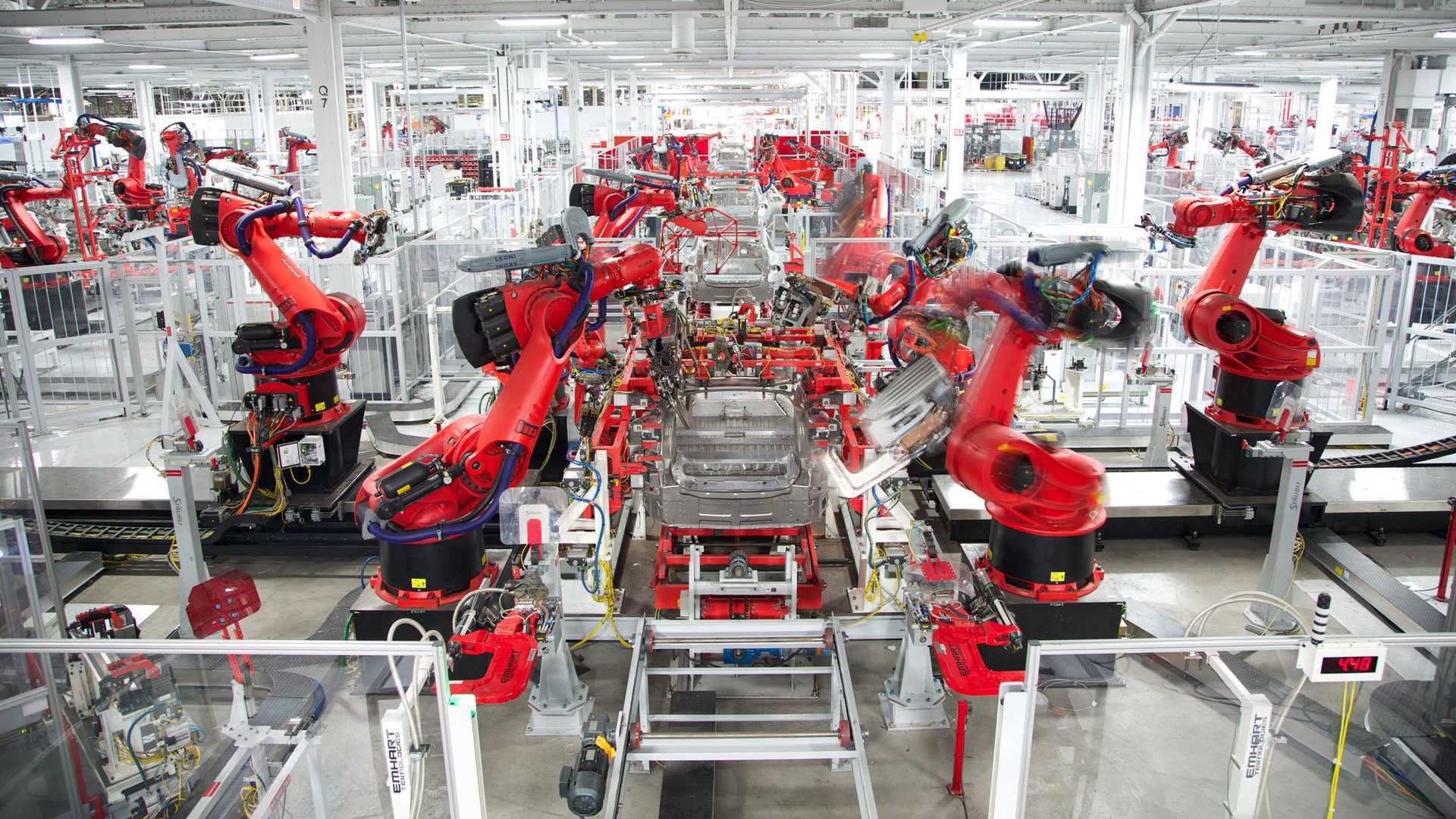

However, China carries excess vehicle manufacturing capacity of epic proportions – they have done this for decades. Fiat for example were at one point selling less than 30000 vehicles per year, yet their domestic partners in China could build 600,000 units in jointly owned plants. Not much has changed since.

The difference? European markets are stable with modest growth, and China’s domestic market is still growing strongly. Investors will forgive many things when growth is strong.

Governments squabble, and the automotive sector withers

Vehicle manufacturing, including all their component suppliers, require a significant amount of cash to invest in buildings, tooling and people. This investment can be moved in a matter of months, but usually a vehicle manufacturer makes products which can be diverted around a region but not always around the world.

Consider a Ford F-150, still a very profitable product for Ford in North America. For Europe the vehicle is so big it exceeds most car parking spaces, and even if it can be parked there’s no space to open the doors. For the dedicated few who import them, they love it and put up with odd inconveniences – high import duties, hefty fuel consumption, left hand drive.

The majority of the USA production is too big, and once exported, too expensive. Europe, like Japan, South Korea and China, builds vehicles which can be exported to more destinations than domestic USA vehicles, because they were engineered for a global market.

European products tend to carry higher than usual prices due to higher labour costs, and more unique tooling investments. The China model follows Japan manufacturing, with a lot of major sub-assemblies shared between multiple brands. This is part of the strategy for reduced cost base – a European manufacturer can pare a low-cost BEV to make cents in profit, yet Chinese based manufacturers still have 20 per cent plus margin at the very same price point.

All of the start-ups (some of which have been ‘start-ups’ for many decades already) have bench marked against Mercedes-Benz, BMW, Audi and Porsche. This is a back handed compliment, but a warning sign that has been ignored for too long. Not innovating enough, allowing costs to creep up and simply getting consumers to believe there is parity between established European brands compared to ‘start-ups’ is not a good place to be. Complacency is the enemy of any business.

China and BRICS just wait

As the own goals between the EU27 Commission and member governments pile up, so profits dwindle as does tax income. This spiral has prompted the EU 27 Commission and one of the 6 Commission Presidents, Ursulla von der Leyen, to spring into action. They have stated they will listen, but none of the punishing rules will change, nor the ‘Net Zero’ ambition.

King Canute. The sea. Can we teil how that ends?

As the EU27 are attacked from China, the USA and internally, China (paying elevated import duties) is paid by EU27 manufacturers to buy carbon credits. Yes. That’s right. European manufacturers are encouraged by the EU Commission to pay the aggressor – who could then pick up the wreckage for less than pennies on the pound when the whole show explodes.

Repairers?

Is the insurer / repairer partnership strong enough to resist the ‘single use vehicle’?

China is set to build more than 32 million vehicles in 2025, about one third of the global production. There is little interest in detailed or intricate repair of the vehicles, even though they have been designed for repair. Why? The economics of BEVs, where repairers capable of restoring a damaged battery are so thin on the ground, insurers write off rather than repair.

Not good for repairers.

Oh – and by the way. Autonomy is still ‘just around the corner’ as it’s been for the past decade…..and won’t eliminate material damage. Nobody has yet perfected a vehicle that is literally driverless unless it runs on a dedicated route. The technology is much, much better than even a few years ago, but if insurers and governments are going to stand behind this, it needs to be perfect.

Well, the end game could be SAE level 5 (‘hop in and tune out’) but the likely end game for around another decade is SAE level 2 or 3. The result? Well, given the massive silence over driver training to get the best out of ‘autonomous systems’ (i.e., super ADAS), the ‘and you now have control’ moment will cause all sorts of personal issues.

Consider aviation. Most commercial airliners have highly automated systems to allow pretty-near automatic landing and take-off. However, pilots are given huge training programmes with frequent updates to ensure they are equipped to make the correct decisions when the ‘and you now have control’ moment arrives.

Driving a vehicle at ground level is demanding, and the idea an SAE level 2 or 3 system is an aid. However, and this requires a different type of concentration to get the best out of the system.

Fear not, for the masses who remain untrained, the underlying ADAS will ensure the impact speed is reduced, but the collision will be exactly, precisely, executed. Woops.

For repairers, one door closes and another opens.

{kind=link}